Beyond Jet Fuel Shortage: Why Aviation Oil and Hydraulic Fluid Are at Risk Next

Jet fuel is grabbing the headlines. But every oil-derived aviation consumable – turbine oils, hydraulic fluids, greases, corrosion inhibitors – shares the same upstream supply chain. Here is what operators should be watching – and doing – right now.

The Headline Everyone Is Reading

As of April 23, 2026, the Strait of Hormuz is effectively closed. Iran-US tensions, combined with tanker insurance rates, have shut down the primary artery for Middle East crude and refined products. Brent crude has spent more than a month above $100 – touching $126 at its peak – and refining capacity outside the Gulf is straining to fill the gap. Jet fuel prices have roughly doubled since March, and Asia-Pacific countries from the Philippines to Sri Lanka are already reporting shortages at the ramp.

The aviation press has been laser-focused on one thing: when airlines will run out of fuel. That is a real question. However, it is not the question that matters most to FBOs, MROs, aviation technicians, and charter operators. Your real exposure is broader, and it has a longer tail.

The Story No One Is Writing Yet

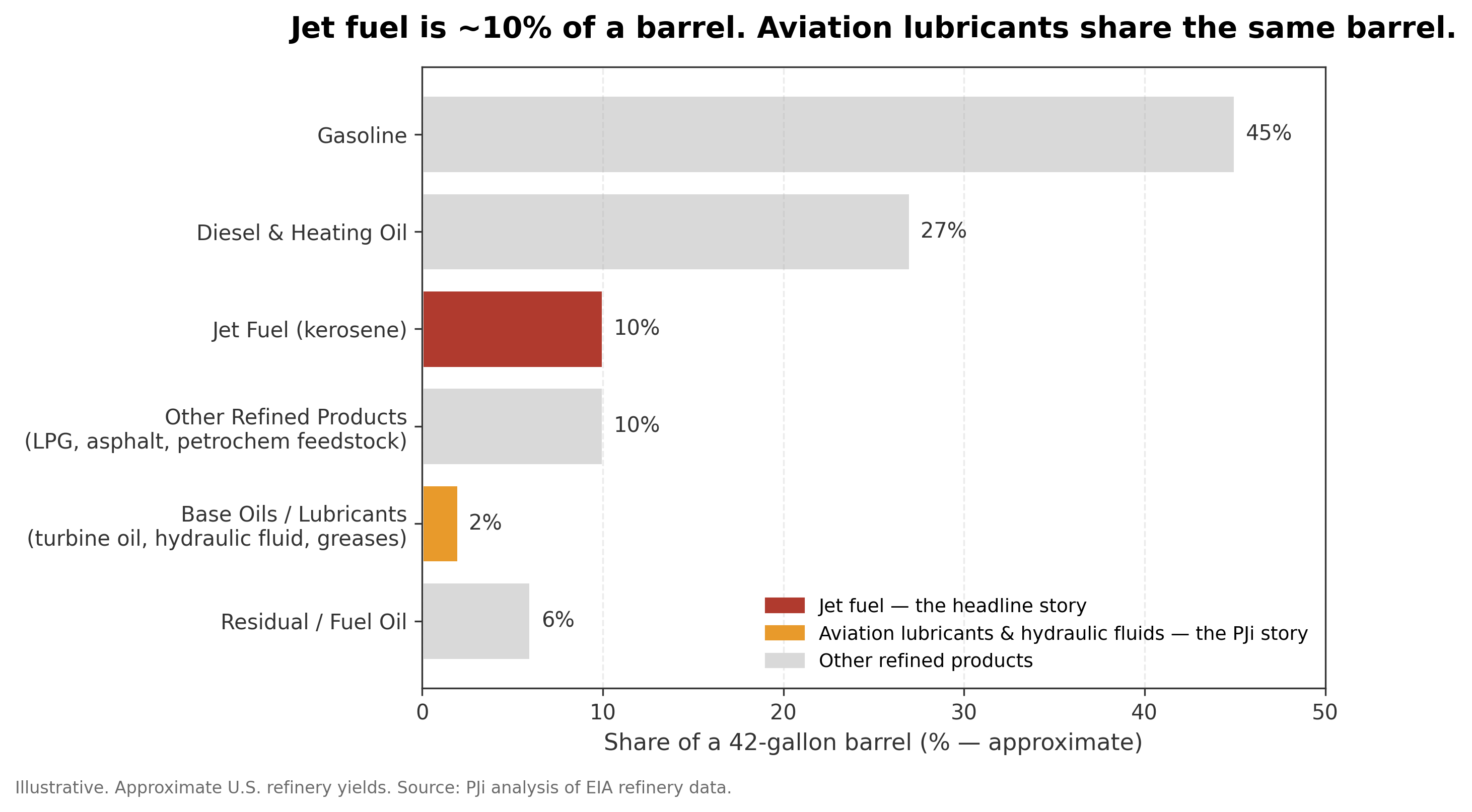

Jet fuel is one product out of a barrel of crude. So are the base oils that go into every turbine engine oil, every piston aircraft oil, every hydraulic fluid bottle on your shelf, every grease gun cartridge, and nearly every can of cleaner, solvent, and corrosion inhibitor in your hangar.

When the upstream barrel gets constrained, every downstream product feels it. Jet fuel gets the press because airlines are visible and vulnerable. Lubricants and hydraulic fluids do not make cable news. But they show up in your ops the week after the fuel story does – in longer lead times, higher quotes, and backorders on products you used to stock without thinking.

Figure 1. Jet fuel is roughly 10% of a refined barrel of crude. Base oils used in aviation lubricants come from the same refining stream, in smaller volume but with more specialized demand. When the barrel tightens, both lines feel it.

What Is Already Moving

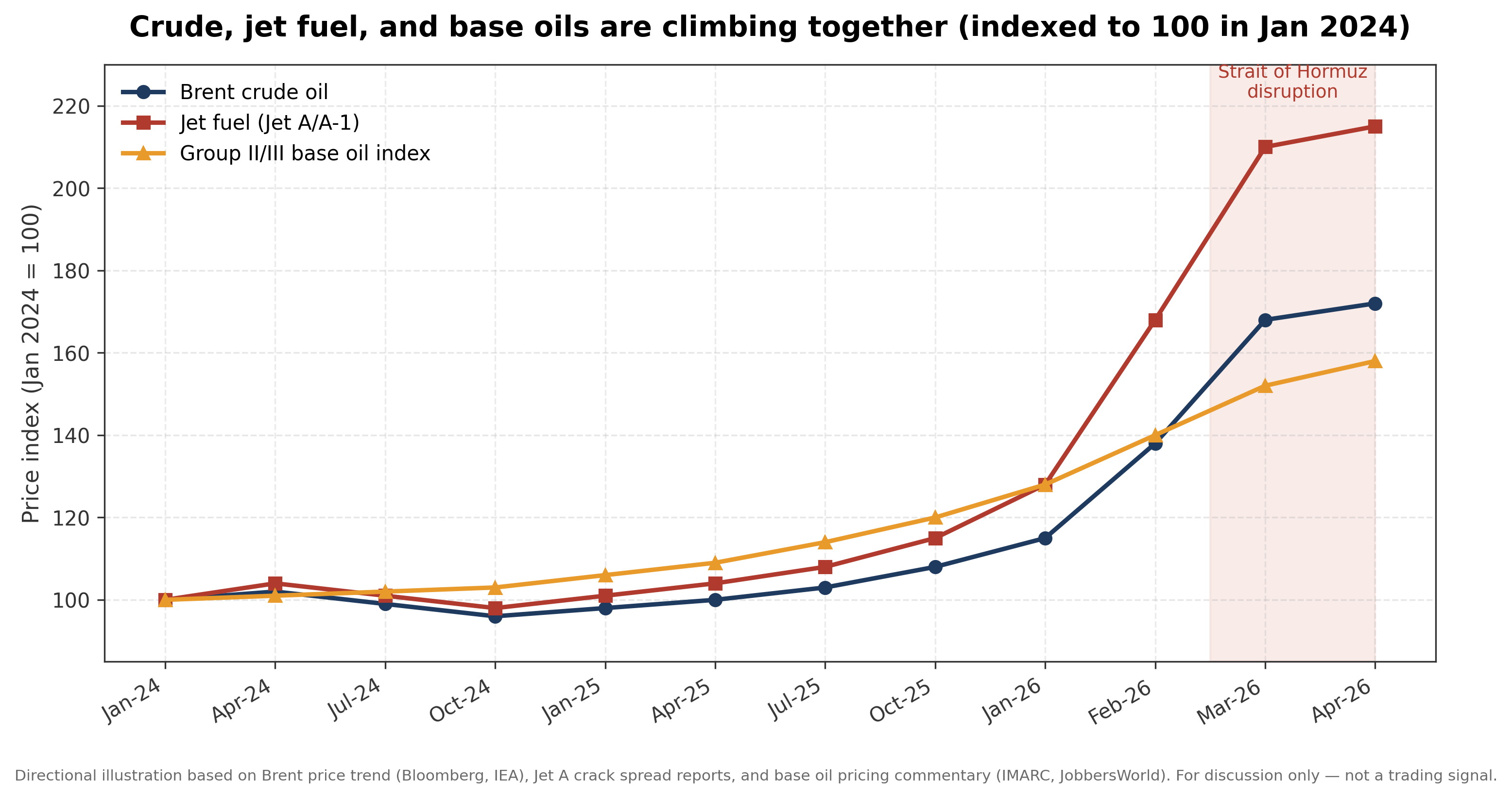

This is not a forecast. The base oil market has already started repricing:

- Q3 2025 saw Group II and Group III base oils – the backbone of modern aviation turbine oils and synthetic hydraulic fluids – surge on tight supply and rising demand, per IMARC Group price tracking.

- In March 2026, JobbersWorld reported base oil and additive price hikes moving through the lubricants supply chain, with industry sources explicitly citing Middle East tensions and crude supply route risk as the trigger.

- Diesel and jet fuel crack spreads have hit records – at times topping $80 per barrel – because jet fuel competes with diesel for refinery priority, and diesel wins almost every time when governments get nervous about gasoline and diesel prices.

Translation: the products PJi sells are already getting more expensive to produce. The only question is how fast that flows through to the landed price and lead time.

Figure 2. Crude, jet fuel, and Group II/III base oils have moved together since the Hormuz disruption. Jet fuel is the sharpest line because refineries are re-prioritizing away from the kerosene band. Base oils lag jet fuel in percentage terms, but the direction is unmistakable.

Your Consumables Supply Chain, Mapped

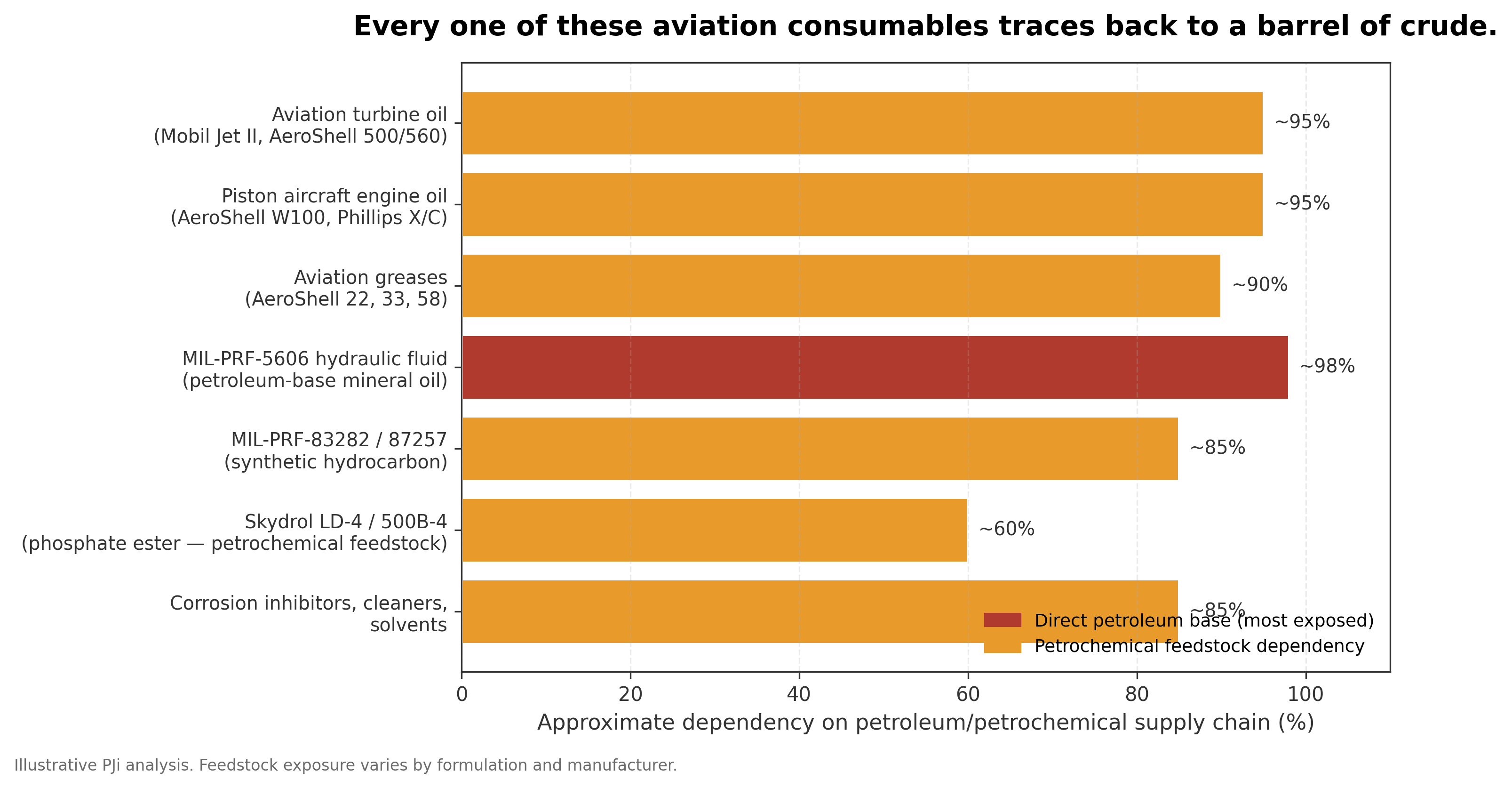

Walk the shelf of any FBO, MRO, or Part 145 shop and almost everything not made of metal traces back to a barrel of crude:

- Aviation turbine oil (Mobil Jet Oil II, AeroShell Turbine Oil 500 and 560, Eastman Turbo Oil 2197) uses highly refined Group II, III, or IV synthetic base stocks – all petroleum-derived.

- Piston aircraft engine oil (AeroShell W100 series, Phillips 66 X/C) is still overwhelmingly mineral-based.

- MIL-PRF-5606 hydraulic fluid is a petroleum-based mineral oil formulation. Direct exposure.

- MIL-PRF-83282 and MIL-PRF-87257 use synthetic hydrocarbon base stock – fewer links back to crude, but the feedstocks still originate in the refinery.

- Skydrol LD-4 and 500B-4 (and HyJet equivalents) are phosphate ester fluids. They are not direct mineral oil products, but their manufacture relies on petrochemical feedstocks that share the same constrained supply chain.

- Aviation greases (AeroShell 22, 33, 58, 64), corrosion inhibitors (ACF-50, CorrosionX, Boeshield), cleaners, and solvents – nearly all petroleum or petrochemical.

Figure 3. A quick audit of your hangar shelf. Every category above depends – directly or through petrochemical feedstocks – on the same refining complex that is now under pressure.

The Risk Operators Are Underpricing

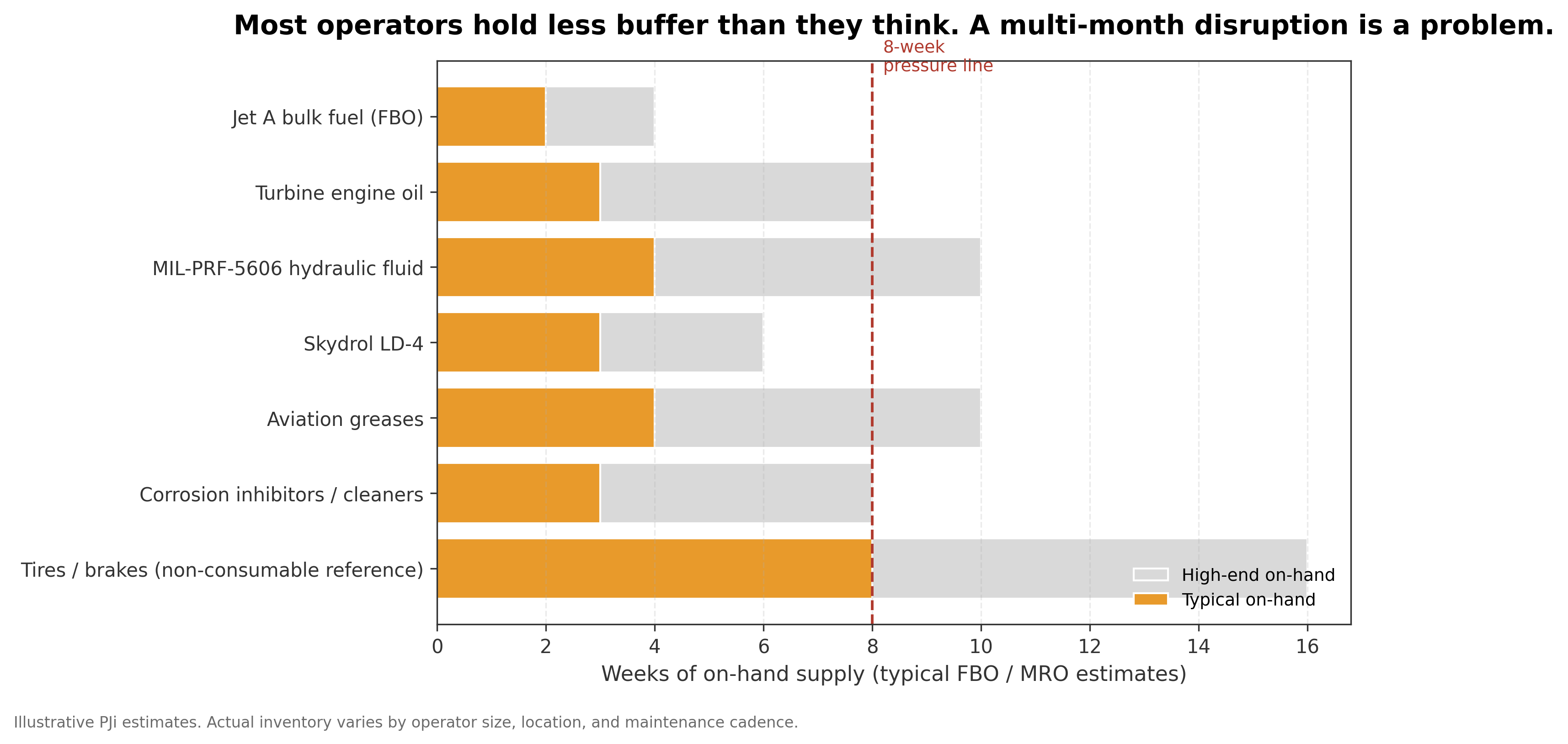

Most FBOs and MROs carry between three and ten weeks of on-hand inventory for common consumables. That is fine for a normal supply chain. It is not fine for a Hormuz disruption that has already run nearly two months and could extend well beyond any political resolution – because the logistics catch-up takes longer than the closure itself.

Figure 4. Typical on-hand coverage for common aviation consumables, illustrative. The 8-week pressure line aligns with the duration of the current disruption. Most operators are inside that buffer, whether they realize it or not.

The Second-Order Risk: Deferred Maintenance

Airlines are the headline buyers of jet fuel. They are also the largest buyers of turbine oils, hydraulic fluids, and greases. When fuel costs spike and margins compress – IATA had net airline margins at 3.9% going into 2026, and that number will move – three things tend to happen in order:

- Capacity is parked. Lufthansa has already announced that older, less fuel-efficient aircraft will be taken out of service and that a feeder airline will be shut down.

- Non-fuel costs come under the microscope. Maintenance intervals get stretched to the edge of the AMM. Service bulletins get re-prioritized. Consumable line items get value-engineered.

- Then reality catches up. Deferred maintenance creates a demand bow-wave on consumables six to twelve months later. Operators that did not stock are paying premium prices to catch up.

FBOs, charter operators, and independent MROs are on the other side of that curve. You cannot defer a turbine oil change the way a scheduled carrier can defer a cabin refurb. And you cannot pass a fuel surcharge along as cleanly as an airline can.

What to Do This Week

This is the practical checklist. None of it is complicated. All of it is time-sensitive.

- Audit your real inventory coverage, not your PAR levels. Pull 90-day usage numbers on turbine oils, 5606, 83282, 87257, Skydrol variants, aviation greases, and corrosion inhibitors. Compare to what is actually on the shelf.

- Extend coverage on the top-10 items now. If you normally carry four weeks, push to eight. If you carry eight, push to twelve. Lead times are lengthening; pricing is not going the other way.

- Lock in pricing where you can. Ask your supplier about quote validity windows. Any quote that is "good for 30 days" is worth more today than it will be in two weeks.

- Review approved substitutes before you need them. Confirm which MIL-SPECs and OEM approvals on your shelf have cross-qualified alternatives. When one brand backorders, you want the substitution research already done.

- Have the conversation with your customers. A two-paragraph email from an FBO or MRO explaining what you are doing to protect parts availability is worth more than any marketing campaign. It also frames price adjustments before they happen.

The PJi View

Jet fuel is not our lane. But the upstream disruption driving the fuel shortage is absolutely ours. Our job is to make sure the FBOs, MROs, technicians, flight schools, maintenance schools, and charter operators we serve do not get caught flat-footed on the consumables that keep aircraft dispatched.

We are not posting this to scare anyone. The message is simpler: jet fuel is the loudest story in the room, and there is a quieter one happening right behind it. The operators who handle the quiet story well will come out the other side with their dispatch reliability intact and their customers more confident than before.

If you want a hand with pressure-testing your consumables coverage or pricing out an extended stock position for any of the products mentioned above, our team is standing by.

Frequently Asked Questions

Why are aviation lubricants and hydraulic fluids exposed to the same supply disruptions as jet fuel?

Jet fuel, turbine engine oils, piston aircraft oils, hydraulic fluids, and aviation greases all originate from the same upstream source: crude oil. When a major supply route like the Strait of Hormuz is disrupted, the constraint moves through the entire refinery chain, not just the jet fuel stream. Base oils – the refined petroleum products that form the foundation of virtually every aviation lubricant and hydraulic fluid – are processed at the same facilities and compete for the same refinery capacity as jet fuel and diesel. As a result, price increases and supply tightening in aviation turbine oil, MIL-spec hydraulic fluid, and aviation grease typically follow a fuel shortage by weeks, not months, making early action by FBOs and MROs essential.

Which aviation consumables are most directly exposed to crude oil supply disruptions?

Aviation consumables with the most direct exposure to petroleum supply risk include mineral-based piston engine oils such as AeroShell W100 and Phillips 66 X/C, MIL-PRF-5606 hydraulic fluid (a direct mineral oil formulation), and aviation turbine oils that rely on Group II, III, or IV synthetic base stocks – all petroleum-derived. Synthetic hydraulic fluids like MIL-PRF-83282 and MIL-PRF-87257 have fewer direct links to crude oil but still depend on petrochemical feedstocks that flow through the same constrained supply chain. Even phosphate ester hydraulic fluids such as Skydrol LD-4 and 500B-4 – though not mineral oil products – rely on petrochemical manufacturing inputs that are subject to the same upstream pressures. Aviation greases, corrosion inhibitors like ACF-50 and CorrosionX, and most hangar cleaners and solvents round out the list of products facing elevated supply risk during a sustained crude oil disruption.

Are phosphate ester hydraulic fluids like Skydrol less vulnerable to petroleum supply disruptions than mineral-based fluids?

Phosphate ester hydraulic fluids – including Skydrol LD-4, Skydrol 500B-4, and HyJet equivalents – are often assumed to be insulated from crude oil supply risk because they are not direct mineral oil products. While they are chemically distinct from MIL-PRF-5606, their manufacture still relies on petrochemical feedstocks and industrial chemical processes that share supply chain infrastructure with petroleum-derived products. During periods of broad upstream disruption, the chemical intermediates used to produce phosphate esters can face their own availability and pricing pressures. Operators running commercial aircraft or turbine-powered fleets that depend on these fluids should not assume immunity from supply tightening and should review their on-hand coverage with the same urgency as those relying on mineral-based hydraulic fluids.

How should FBOs, MROs, and charter operators adjust their consumables inventory strategy during an extended supply chain disruption?

During normal supply chain conditions, three to ten weeks of on-hand inventory for aviation consumables is generally sufficient for most FBO and MRO operations. When upstream disruptions are prolonged – as is the case with a sustained Strait of Hormuz closure – that buffer can disappear faster than procurement teams expect, because lead times lengthen before price increases fully materialize. Aviation maintenance operations should audit 90-day usage data for high-turnover items, including turbine oils, hydraulic fluids, aviation greases, and corrosion inhibitors, then extend coverage to at least eight to twelve weeks on the most critical products. Locking in pricing with suppliers while quotes are still valid, and pre-researching approved substitute products before a primary brand backorders, are two additional steps that can significantly reduce both cost exposure and dispatch disruption.

What is the deferred maintenance demand wave, and why does it create a secondary risk for smaller aviation operators?

When fuel costs spike and airline margins compress, large carriers typically respond by parking older aircraft, stretching maintenance intervals to the limits permitted by the Aircraft Maintenance Manual, and reducing discretionary consumable spending – effectively deferring demand. Six to twelve months later, that deferred maintenance creates a concentrated surge in demand for turbine oils, hydraulic fluids, greases, and other aviation consumables, hitting the market at the same time supply chains are already under pressure. FBOs, independent MROs, and charter operators cannot absorb this wave the way airlines can: they cannot defer turbine oil changes, pass fuel surcharges to customers as cleanly, or leverage the bulk purchasing power that major carriers use to secure priority allocation. Smaller aviation operations that stock strategically ahead of this secondary demand surge – rather than reacting to it – are far better positioned to maintain dispatch reliability and protect customer relationships when consumable availability tightens across the industry.